2019-20 nine-month revenues

2019-20 nine-month revenues

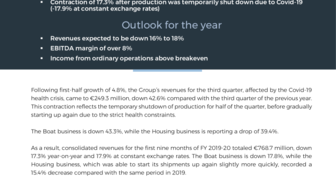

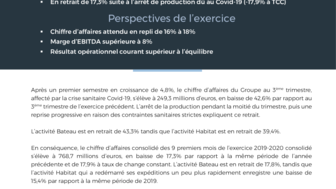

- Contraction of 17.3% after production was temporarily shut down due to Covid-19

(-17.9% at constant exchange rates)

Outlook for the year

- Revenues expected to be down 16% to 18%

- EBITDA margin of over 8%

- Income from ordinary operations above breakeven

Following first-half growth of 4.8%, the Group’s revenues for the third quarter, affected by the Covid-19 health crisis, came to €249.3 million, down 42.6% compared with the third quarter of the previous year. This contraction reflects the temporary shutdown of production for half of the quarter, before gradually starting up again due to the strict health constraints.

The Boat business is down 43.3%, while the Housing business is reporting a drop of 39.4%.

As a result, consolidated revenues for the first nine months of FY 2019-20 totaled €768.7 million, down 17.3% year-on-year and 17.9% at constant exchange rates. The Boat business is down 17.8%, while the Housing business, which was able to start its shipments up again slightly more quickly, recorded a 15.4% decrease compared with the same period in 2019.

For the first nine months, Boat revenues came to €623.2 million, down 17.8% year-on-year and 18.4% at constant exchange rates.

As all of the Group’s plants were temporarily shut down due to the health risks, the contraction in revenues concerns all the segments and regions, which all show a downturn in business at end-May 2020, with the exception of fleet sales, which are up 26.8%, thanks to an excellent first half of the year (+60%).

On a reported basis, North America (-22.4%) was slightly less affected than Europe (-26.6%), despite a significant drop of -46.6% for the American brands. The contraction for other regions around the world came to -19.5%.

For the first nine months of the year, the downturn for motorboat segments (-21.7%) shows contrasting trends: the decline was limited for 30 to 60-foot outboard and inboard motorboats, but significantly more marked for the inboard (under 30 feet and over 60 feet) and jet segments.

Sailing revenues are down 13.5%, offset in particular by the fleet sales performance mentioned previously.

At end-May 2020, the Sailing and Motorboat segments each represent 50% of revenues for the Boat division.

For the first nine months of the year, the Housing division recorded €145.3 million of revenues, down 15.4% compared with the first nine months of the previous year.

The positive first-half trends (+5.4%) were brought to a sudden stop by the suspension of production in the third quarter, which saw a 39.4% drop in revenues for the Housing division (€48.3 million) compared with the third quarter of the previous year.

The gradual resumption of operations, ramped up from early May, will not be sufficient to make up for the lack of production during the six weeks of the shutdown. Combined with the order cancellations and deferrals recorded by the Boat business, particularly from charter firms, 2019-20 full-year revenues are expected to contract by 16% to 18% on a reported basis compared with the previous year.

The Housing division expects its full-year revenues to come in 13% to 14% lower than 2018-19.

In this context, the Group estimates that its full-year revenues will contract by 16% to 18% on a reported basis, with an EBITDA margin of over 8% and income from ordinary operations above breakeven.

The next key dates will be:

- July 9, 2020 at 6pm: presentation of the core features of the Group’s strategic plan “Let’s Go Beyond!” for 2020-2025

- September 8, 2020: new boat models announced for the 2020-2021 season

- October 27, 2020: 2019-20 full-year earnings released

At constant exchange rates: change calculated based on figures for the first half of 2019-20 converted at the exchange rate for the first half of 2018-19.

EBITDA: earnings before interest, taxes, depreciation and amortization, i.e. operating income restated for allocation / reversal of provisions for liabilities and charges, depreciation charges and IFRS GAAP (IFRS 2 and IAS 19).

Free cash flow: cash generated by the company during the reporting period before dividend payments, changes in treasury stock and the impact of changes in scope.

Net cash: cash and cash equivalents after deducting financial debt and borrowings, which include IFRS 16 lease liabilities and financial liabilities on commitments to buy out non-controlling interests.

Income from ordinary operations adjusted for currency hedging: income from ordinary operations after taking into account currency hedging income and expenses. Income from ordinary operations adjusted for currency hedging is an alternative performance indicator that makes it possible to measure the Group’s performance after the impact of foreign exchange hedging. Since 2016, income and expenses from currency hedging primarily reflect the difference between forward purchase / sales positions and the accounting exchange rate for recording transactions in currencies (USD, PLN). The Group hedges its commercial currency risk based exclusively on currency forwards.

This press release, which has been prepared by BENETEAU SA (the “Company”, and together with its subsidiaries and affiliates, the “Group”), does not constitute, and should not be constructed as, an offer to sell or the solicitation of an offer to purchase or subscribe for any securities of the Group in any jurisdiction.

This press release may include forward-looking statements. By their nature, forward-looking statements involve risks and uncertainties, which could cause the actual results and performance of the Group to be materially different from the future results and performance expressed or implied by such forward-looking statements.

About Groupe Beneteau

Founded in Vendée 140 years ago by Benjamin Bénéteau, Groupe Beneteau is today a world leader in the boating industry. With an international industrial presence spanning 16 production sites and a worldwide commercial network, the Group generated revenue of €849 million in 2025 and has a workforce of more than 6400 employees mainly in France, United States, Poland, Italy, Portugal, and Tunisia.

True to its mission – Bringing dreams to water – Groupe Beneteau designs and builds boats and services to make every experience on the water truly unique. Through its nine brands, its Boat division offers more than 135 boat models craft to meet the diverse needs and sailing projects of its customers, whether sailing or motoring, monohull or catamaran . Through its Boating Solutions division, the Groupe Beneteau is also involved in services covering daily or weekly boat hire, marinas, the digital sector and financing.

Assets

09 July 2020

200709 BENETEAU CP CA-T3-9mois FR.pdf

Discover also

Management & experts linked