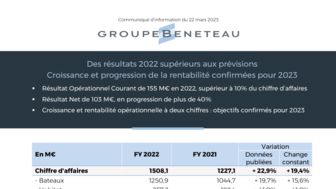

2022 results higher than forecast - Growth and increase in profitability confirmed for 2023

- Income from ordinary operations of €155m in 2022, representing more than 10% of revenues

- Net income of €103m, with over 40% growth

- Double-digit operational profitability and growth: objectives confirmed for 2023

|

€m |

FY 2022 |

FY 2021 |

Change |

|

|

Reported data |

Constant exchange rates |

|||

|

Revenues |

1,508.1 |

1,227.1 |

+ 22.9% |

+ 19.4% |

|

- Boats |

1,250.9 |

1044.7 |

+ 19.7% |

+ 15.6% |

|

- Housing |

257.2 |

182.4 |

+ 41.0% |

+ 41.0% |

|

EBITDA |

229.2 |

181.6 |

+ 26.2% |

+ 9.1% |

|

% EBITDA / revenues |

15.2% |

14.8% |

+0.4 pts |

|

|

- Boats |

198.8 |

163.4 |

+ 21.7% |

|

|

- Housing |

30.4 |

18.3 |

+ 66.7% |

+ 2.7% |

|

Income from ordinary operations |

154.7 |

95.8 |

+ 61.5% |

+ 29.3% |

|

% income from ordinary operations / revenues |

10.3% |

7.8% |

+2.5 pts |

|

|

- Boats |

131.8 |

84.7 |

+ 55.7% |

|

|

- Housing |

22.8 |

11.1 |

+ 105.9% |

|

|

Net income (Group share) |

103.1 |

73.4 |

+ 40.5% |

+ 19.3% |

|

Free cash flow |

28.3 |

176.3 |

|

+ 105.9% |

|

Net cash |

211.2 |

222.4 |

|

|

Thanks to an excellent fourth quarter, Groupe Beneteau closed out FY 2022 with revenues of €1,508m, up 22.9% based on reported data compared with 2021. This performance reflects the outstanding growth achieved by both the Boat division and the Housing division.

Ordinary operating margin of over 10% from 2022

Full-year income from ordinary operations came to €154.7m for 2022, representing 10.3% of revenues, up 61.5% from 2021 (€95.8m). This +2.5 point improvement in the ordinary operating margin is consistent across both divisions (Boats +2.4 pts to 10.5% and Housing +2.8 pts to 8.9%). This reflects the combined impacts of the increase in activity for the Boat and Housing divisions (+€21m), the continued reduction in depreciation (+€5m) and the operational performance achieved by the teams, which made it possible to limit the impact of the supply chain disruption and inflation (+€13m). This result also factors in the favorable change in exchange rates during the year (+€31m), as well as the launch costs for a new industrial unit set up in Portugal (-€5m) and the treatment as expenses of development costs relating to a new ERP using SaaS software (-€6m).

Consolidated EBITDA[1] climbed to €229.2m, representing 15.2% of revenues (vs. 14.8% in 2021), up 26.2%.

Net income growth of 40.5%, with €211m of net cash

Net income came to €103.1m for FY 2022, up 40.5% compared with 2021. It includes -€12.3m of financial income and expenses (vs. -€2.5m in 2021), linked primarily to currency hedging income and expenses (-€10m), resulting from the change in euro-dollar exchange rates during the year.

For the year, the share of associates represents a -€2.4m expense. The robust development of the charter and boat club markets in 2022 enabled the three companies in which the Group has been a shareholder since 2021 to achieve 27% growth in their full-year revenues, which are now back up to pre-Covid levels, combined with an €11m increase in their net income.

The Group’s shareholders’ equity represented €706m at December 31, 2022, compared with €630m at December 31, 2021.

Free cash flow generated during the year totaled €28m. This includes a normalization of finished product inventory levels (+€83m) and an increase in stock levels covering raw materials (+€27m). Net investments totaled €69m, coming in €9m higher than the level of depreciation for the year. They include the finalization of the plan to restart the Sainte-Hermine site for the Housing business (€6.6m).

Net cash, following €24.5m of dividend payments, totaled €211m at December 31, 2022.

Lastly, the return on capital employed (ROCE1) represented 32% at December 31, 2022 (vs. 24% at December 31, 2021 and 14% at August 31, 2019). This increase reflects the improvement in operational profitability, the rationalization of investment strategies and the effective management of working capital requirements.

B-SUSTAINABLE CSR plan ramping up

Presented on December 5, 2022, the Group’s CSR program B–SUSTAINABLE is built around three pillars: Engaged Crew, Preserved Oceans and Ethical Growth.

One of the core priorities with the Engaged Crew pillar is the workplace accident frequency rate, which shows a very strong improvement for 2022, despite a context of high recruitment levels. The frequency rate for accidents resulting in time off work fell by more than 25% in 2022 compared with 2021. This represents a reduction of more than 50% since a proactive approach was rolled out in all of the Group’s facilities in 2016. In view of the progress made, a new target for a further 15% reduction has been set for the next three years.

Concerning the Preserved Oceans pillar, the Group reduced the intensity of direct CO2 equivalent emissions (Scope 1&2) per thousand hours worked by 14% in 2022 compared with 2021. The Group has now completed two lifecycle analyses of the Boat division’s products. They are helping the Group draw up its innovation plan, which aims to offer alternative propulsion solutions across its entire portfolio by 2030, while gradually incorporating recycled resins into the industrialization of its boats.

Lastly, as part of the stakes involved with the Ethical Growth pillar, the Group would like to engage the entire industry around a sustainable development approach. By linking up with Ecovadis, an international firm specialized in solutions for assessing responsible purchasing and CSR performance, the Group aims to ensure that the majority of its suppliers are certified by 2025.

“The robust development of all the markets that the Group operates on, the quality of its product offering, and the excellent operational execution achieved despite the supply chain disruption that affected the entire industry enabled Groupe Beneteau to set two historic records, with over €1.5bn of revenues and €150m of income from ordinary operations. I would like to thank all of the Group’s teams. They have once again showed extraordinary levels of commitment and dedication to achieve the initial ambition from our Let’s Go Beyond! strategic plan from 2022. The Group is therefore perfectly positioned to achieve its new objective looking ahead to 2025”, confirms Bruno Thivoyon, Chief Executive Officer.

GROWTH AND PROFITABILITY CONFIRMED FOR 2023

Boats: premiumization and increase in profitability confirmed

The 20 new models presented in 2022 are helping drive growth in the order book, while dealership inventory is back up to pre-Covid levels. In this context, the Boat division is expected to record revenue growth of over 10% at constant exchange rates in 2023.

The Sailing business is benefiting from very strong demand for catamarans, linked in particular to the commercial success of the new LAGOON 51 and 55 models, as well as the launch of the EXCESS 14. Alongside this, demand for monohull sailing models is being supported by the launches of the FIRST 44, OCEANIS 60 and JEANNEAU YACHTS 55.

For the Motor business, the launch of the JEANNEAU DB (37 and 43), WELLCRAFT Adventure (355 and 435) and PRESTIGE Multihull (M48 and M8) ranges will enable the Group to move into new segments and continue rolling out its premiumization strategy.

This strategy will enable the Boat division to continue to increase its ordinary operating margin, which is expected to reach over 10.5% in 2023, higher than 2022, which benefited from particularly favorable exchange effects.

Housing: heading set for €300m of revenues

The Housing division is expected to record over 15% growth in France and across the European market, paving the way for it to achieve revenues of nearly €300m in 2023. The ordinary operating margin is expected to be over 9.5%, up +0.6 points versus 2022.

Group in 2023 in line with the heading set for 2025

Groupe Beneteau expects to generate more than €1,660m of revenues in 2023, thanks to over 10% growth compared with 2022. Income from ordinary operations is expected to come in higher than €170m, representing 10.3% of revenues, in line with the new profitability target presented on December 5, 2022.

This forecast could be exceeded if the supply chain disruption continues to ease.

The growth and the increase in profitability for the charter and boat club activities are expected to be reflected in a positive contribution by associates in 2023.

Inclusion in the SBF 120

On March 20, 2023, Groupe Beneteau joined the SBF 120, one of the Paris stock market’s leading indices that groups together the top 120 companies listed on Euronext Paris in terms of liquidity and market capitalization. This decision by Euronext’s Expert Indices Committee on March 9, 2023 follows the quarterly review of the Euronext Paris indices.

*

* *

PROPOSED DIVIDEND

Groupe Beneteau’s Board of Directors has decided to submit a dividend of €0.42 per share for approval at the Combined General Meeting on June 15, 2023, up 40% compared with the dividend of €0.30 per share paid in 2022.

Groupe Beneteau will report its 2023 first-quarter revenues on May 10 (after close of trading).

*

* *

A detailed presentation of the full-year business and financial results is available on the Groupe Beneteau website.

The annual and consolidated financial statements presented here, as reviewed by the Board of Directors on March 21, 2023, are currently being audited and will be definitively approved for the publication of the annual financial report by the end of April. The Board of Directors will approve the accounts on April 25, 2023.

Cash position

|

€m |

2022 |

2021 |

|

Reported data |

Reported data |

|

|

Operating cash flow |

175.3 |

148.9 |

|

Net cash flow from investments |

-69.4 |

-50.7 |

|

Change in working capital |

-75.6 |

83.7 |

|

Other |

-2.0 |

-5.5 |

|

Free cash flow |

28.3 |

176.3 |

|

Dividends / treasury stock |

-38.5 |

1.0 |

|

Change in scope |

-0.1 |

-47.9 |

|

Change in net cash |

-10.3 |

129.3 |

|

Opening net cash adjustment |

-0.9 |

-0.4 |

|

Opening net cash position |

222.4 |

93.4 |

|

Closing net cash position |

211.2 |

222.4 |

ROCE

|

€m |

2022 |

2021 |

2019 |

|

(Dec 31) |

(Dec 31) |

(Aug 31, 2019) |

|

|

Revenues |

1,508.1 |

1,227.1 |

1,336.2 |

|

Income from ordinary operations |

154.7 |

95.8 |

82.0 |

|

% income from ordinary operations |

10.3% |

7.8% |

6.1% |

|

Capital employed |

488.5 |

400.2 |

571.3 |

|

Net fixed assets |

336.1 |

323.0 |

373.8 |

|

Goodwill |

91.0 |

90.8 |

91.1 |

|

Working capital requirements |

61.3 |

-13.5 |

106.4 |

|

ROCE |

32% |

24% |

14% |

At constant exchange rates: change calculated based on figures for the period from January 1 to December 31, 2022 converted at the exchange rate for the same period in 2021 (January 1 – December 31, 2021).

EBITDA: Earnings before interest, taxes, depreciation and amortization, and IFRS 2 and IAS 19 adjustments following IFRS GAAP, i.e. income from ordinary operations restated for allocation / reversal of provisions for liabilities and charges, depreciation charges and IFRS GAAP (IFRS 2 and IAS 19).

ROCE: Return on capital employed, i.e. the ratio between income from ordinary operations and the level of capital employed (net fixed assets including goodwill + working capital requirements).

Free cash flow: Cash generated by the company during the reporting period before dividend payments, changes in treasury stock and the impact of changes in scope.

Net cash: Cash and cash equivalents after deducting financial debt and borrowings, excluding financial debt with floor plan-related financing organizations.

About Groupe Beneteau

Founded in Vendée 140 years ago by Benjamin Bénéteau, Groupe Beneteau is today a world leader in the boating industry. With an international industrial presence spanning 16 production sites and a worldwide commercial network, the Group generated revenue of €849 million in 2025 and has a workforce of more than 6400 employees mainly in France, United States, Poland, Italy, Portugal, and Tunisia.

True to its mission – Bringing dreams to water – Groupe Beneteau designs and builds boats and services to make every experience on the water truly unique. Through its nine brands, its Boat division offers more than 135 boat models craft to meet the diverse needs and sailing projects of its customers, whether sailing or motoring, monohull or catamaran . Through its Boating Solutions division, the Groupe Beneteau is also involved in services covering daily or weekly boat hire, marinas, the digital sector and financing.

Media contact

Clarence Duflocq

Dir. Investor Relations & ESG Coordination

+33 / (0)2 51 26 88 50

c.duflocq@beneteau-group.com

Assets

22 March 2023

230322 BENETEAU PR FY2022Earnings EN

22 March 2023

230322 BENETEAU Presentation FY2022Earnings EN

22 March 2023

230322 BENETEAU CP ResultatsAnnuels2022 FR

22 March 2023

230322 BENETEAU Presentation ResultatsAnnuels2022 FR

Discover also

Management & experts linked