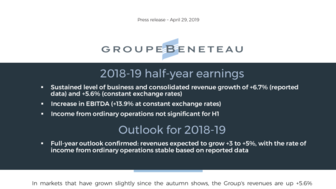

2018-19 half-year earnings

- Sustained level of business and consolidated revenue growth of +6.7% (reported data) and +5.6% (constant exchange rates)

- Increase in EBITDA (+13.9% at constant exchange rates)

- Income from ordinary operations not significant for H1

- Full-year outlook confirmed: revenues expected to grow +3 to +5%, with the rate of income from ordinary operations stable based on reported data

In markets that have grown slightly since the autumn shows, the Group's revenues are up +5.6% (constant exchange rates) for the first half of the financial year, thanks to a sustained level of business across both the Boat and Housing divisions.

EBITDA is up +13.9% at constant exchange rates, in line with the Group’s sustained rate of investment. As billing is concentrated primarily over the second half of the year, income from ordinary operations is negative at the end of the first half of this year, as expected in line with previous years.

At March 31, 2019, the order book for the Boat business is up +4.3% based on reported data (+2.9% at constant exchange rates). For the Housing business, the order book is down 4.5%.

***

A detailed presentation of the half-year earnings is available at the bottom of this webpage.

The half-year activity report will be available from April 30, 2019 at the bottom of this webpage.

The next announcement is scheduled for July 11, 2019, when revenues for the first nine months of FY 2018-19 will be reported.

|

€m |

H1 2018-19 |

H1 2017-18 |

Change |

||||||

|

(reported data) |

(constant exchange rates) |

||||||||

|

Revenues |

495.9 |

464.9 |

+6.7% |

+5.6% |

|||||

|

- Boats |

403.8 |

378.0 |

+6.8% |

+5.6% |

|||||

|

- Housing |

92.1 |

86.9 |

+6.0% |

+6.0% |

|||||

|

EBITDA* |

32.5 |

26.1 |

+24.5% |

+13.9% |

|||||

|

Income from ordinary operations |

-3.4 |

-4.4 |

ns |

|

|||||

|

Net income (Group share) |

-1.6 |

0.1 |

ns |

|

|||||

|

Closing net cash position |

-98.9 |

-53.9 |

|

||||||

* EBITDA: earnings before interest, taxes, depreciation and amortization, i.e. operating income restated for allocation / reversal of provisions for liabilities and charges and depreciation charges.

For the first half of 2018-19, consolidated revenues climbed to €495.9m, up +5.6% at constant exchange rates compared with the first half of the previous year and +6.7% based on reported data.

Income from ordinary operations improved by €1m to -€3.4m, while net income is down €1.7m to -€1.6m with the impact of currency hedging (-€2.4m for the period, versus +€2.4m for the first half of 2017-18) and tax (+€2.1m versus +€1m for the first half of 2017-18).

For the first half of 2018-19, the Boat Division generated revenues of €403.8m, up +5.6% at constant exchange rates compared with the first half of the previous year and +6.8% based on reported data. In a global market on which growth is now between 2% and 3%, the Group’s revenues are continuing to grow at twice the market rate.

The Boat Division’s growth is being driven by the European brands’ good results on the North American markets and by fleets, with multihulls making strong progress. Sales in Continental Europe are continuing to progress, while certain markets such as the UK and Turkey have contracted sharply, resulting in a slight drop in sales for the European region overall. Sales for the Asia-Pacific region are down, in markets with low activity levels. Buoyed by growth in fleet sales and the completion of the Figaro Beneteau 3 program, the percentage of sailing yachts is up 6 points to 50% of the Boat Division’s revenues for the first half of the year.

The progress with EBITDA reflects the policy to invest in and further strengthen the product offering. The Boat Division’s income from ordinary operations came to -€11m, compared with -€11.9m the previous year.

The continued progress with the Transform to Perform plan is reflected in:

- Additional support costs for €4.1m (including indirect production labor, R&D and sales costs);

- Costs linked to the launch of new activities for €1.6m (including the Band of Boats digital platform and Beneteau Boat Club);

- Allocations for investments for €2.6m (primarily for products, including the development of the Excess multihull range with five models, the development of the Sun Loft 47 and the construction of the first two Excess 12 and 15 boats, which will be released over the next year).

The impact of the euro-dollar exchange rate on income from ordinary operations is positive, coming in at €2.7m.

For the first half of 2018-19, Housing Division revenues totaled €92.1m, up 6% compared with the first half of the previous year. This increase is linked primarily to a slight time-lag effect with seasonality, with orders and deliveries recorded earlier in the year.

Income from ordinary operations represents €7.7m, compared with €7.5m the previous year, up 2.3%. This increase in operating income is mainly linked to the growth in volumes delivered at end-February.

In the current market environment, the Group is continuing to forecast consolidated revenue growth of around +2% to +4% at constant exchange rates and +3% to +5% on a reported basis. The rate of income from ordinary operations to revenues is expected to be stable based on reported data.

The Boat Division is forecasting full-year revenue growth of 4 to 6% (reported data).

The Housing Division expects its full-year revenues to contract slightly, due to the slowdown on the French Leisure Homes market, which represents almost 85% of the Division’s market. Sales in Italy, Benelux and Spain are expected to see growth. The rate of operating income is expected to come in slightly lower than the previous year. For reference, the Residential Housing business is no longer active in 2018-19.

At constant exchange rates: change in an item calculated by converting the figures for the first half of 2018-19 based on the rates for FY 2017-18.

EBITDA: earnings before interest, taxes, depreciation and amortization, i.e. operating income restated for allocation / reversal of provisions for liabilities and charges and depreciation charges.

Free cash flow: cash generated by the company during the reporting period before dividend payments and changes in treasury stock.

Net cash: cash and cash equivalents after deducting financial debt and borrowings.

Income from ordinary operations adjusted for currency hedging: income from ordinary operations after taking into account currency hedging income and expenses. Income from ordinary operations adjusted for currency hedging is an alternative performance indicator that makes it possible to measure the Group’s performance after the impact of foreign exchange hedging. Since 2016, income and expenses from currency hedging primarily reflect the difference between forward purchase / sales positions and the accounting exchange rate for recording transactions in currencies (USD, PLN). The Group hedges its commercial currency risk based exclusively on currency forwards.

About Groupe Beneteau

Founded in Vendée 140 years ago by Benjamin Bénéteau, Groupe Beneteau is today a world leader in the boating industry. With an international industrial presence spanning 16 production sites and a worldwide commercial network, the Group generated revenue of €849 million in 2025 and has a workforce of more than 6400 employees mainly in France, United States, Poland, Italy, Portugal, and Tunisia.

True to its mission – Bringing dreams to water – Groupe Beneteau designs and builds boats and services to make every experience on the water truly unique. Through its nine brands, its Boat division offers more than 135 boat models craft to meet the diverse needs and sailing projects of its customers, whether sailing or motoring, monohull or catamaran . Through its Boating Solutions division, the Groupe Beneteau is also involved in services covering daily or weekly boat hire, marinas, the digital sector and financing.

Assets

29 April 2019

190429 BENETEAU Half-year earnings H1-2018-19 EN

29 April 2019

190429 BENETEAU Resultats S1-2018-2019 FR

29 April 2019

190429 BENETEAU Presentation_Resultats S1-2019 FR

30 April 2019